Market Outlook

August 1, 2026

Inflation Affects Us Differently; Your Asset Allocation Matters

Last week’s one-day swoon by stocks (and bonds) was the result of several concerns including inflation. Not so much current inflation, but future inflation fueled by many things, especially energy and food, as well as housing, insurance and health care.

As we often note, the Fed’s preferred inflation gauge (which we’ll return to in just a bit) is the Personal Consumption Expenditures price index (or PCE). Currently at 3.7% year-over-year, that’s significantly above the Fed’s long-term target of 2%. Notably, it hasn’t been below that level since the Pandemic (2000 to 2022) when the global economy shut down. Immediately thereafter, fiscal and monetary stimuli, coupled with severe supply-chain disruptions, sent inflation soaring to a high of 7.0% in June 2022, though it has been falling erratically ever since.

If the trend is our friend, what’s the worry now? Again, whether one uses PCE or the more commonly quoted CPI (which is actually the same measure as CPI-U), 3.5% headline inflation means rising prices continue to weigh especially heavily on two key demographics: young families and retirees. My focus here is the latter.

The good news for America’s seniors (over 70) is — from a collective standpoint — that they’re the wealthiest in history. Stock market gains and home appreciation have grown their aggregate assets to approximately $60 trillion. That’s a third of the nation’s household wealth, up from an estimated 19% share in 1989. While decades of inflation has contributed to that growth, over the past 40 years, asset appreciation has far outpaced consumer inflation. By comparison, inflation-adjusted wealth has left the Baby Boomer generation 133% wealthier than the Greatest Generation. While that suggests that America’s seniors are better prepared financially for retirement, they are also living longer (on average, 3 to 5 years), though their health is not always better for those extra years.

And that takes us to an even deeper financial concern: While many believe that inflation is under-estimated by most practical measures, seniors experience inflation in far different ways than say younger, healthier Americans. And it’s not just a matter of health care costs.

A recent survey and related study by The Senior Citizens League (TSCL) contends that 73% of its respondents in 2024 believe that their Social Security adjustment (COLA) underestimated actual inflation (as measured by CPI-W).

The study further estimates "that Social Security benefits lost about 13.7% of their value from 2016 to 2026 and are now worth about 86 cents on the dollar compared to 10 years ago." It concludes that "to restore their value to 2016 levels, [benefits] would need to rise 15.8%, or $295.85 per month for the average beneficiary."

At the risk of getting too far into the inflation "weeds," economists at the Bureau of Labor Statistics have long understood that inflation differs among demographic groups.

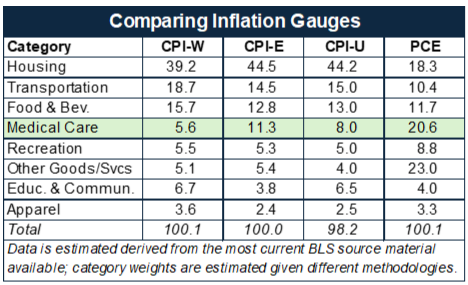

In 1983, it created the CPI-E to better measure the price pressures on people age 62 and older. While it and CPI-W sample the same baskets of goods and services, health care is an 11.3% weight in CPI-E versus 5.6% for CPI-W.

On the other hand, the Fed’s preferred PCE gauge, which captures Medicare, Medicaid and employer-paid premiums, has a 20.6% weight in health care. Arguably, it’s a better gauge for measuring "senior inflation."

Beyond higher health care needs, seniors face other financial pressures. While many younger individuals are contending with historically high housing costs, sometimes the weight of student loans, and day care, older Americans (79% of whom own their own homes) often struggle to maintain them while property taxes can outpace inflation. To that end, The Senior Citizens League has constructed what it believes is a more sensitive gauge of senior inflation which, if implemented last year, would have increased Social Security’s COLA to 3.2% versus 3.0% for CPI-E and the actual increase of 2.8% which is derived from CPI-W. Of course, with Social Security projected to be insolvent in just seven years and perhaps force a 23% reduction in benefits for 70 million recipients, it seems that any plan to turbo-charge benefits would be a long shot.

Retirement StrategiesThough I risk sounding like the sky is falling, the immutable math driving the concerns over Social Security’s long-term viability and a national balance sheet exploding indebtedness to $40 trillion (now larger than the country’s GDP) suggests a certain amount of trouble down the road. But just as you have spent a lifetime preparing for retirement, there are some asset allocation steps to consider within your retirement years.

The first is to consider TIPS, otherwise called Treasury Inflation-Protected Securities. Fidelity makes that easy to do via its Inflation-Protected Index fund. We detailed how it works in the April newsletter (which is posted on our website), but suffice it to say that its name tells you what it does: provides some hedge against inflation as measured by CPI.

You might also consider a buy-and-hold stake in Select Health Care. Over time, this strategy might prove to be an equity hedge against the very area of your life where you can reasonably expect costs to outstrip your income. A diversified stock fund should also accomplish this, but slightly overweighting the S&P 500’s 9% health care weight may make some sense.

To reiterate that point, do not abandon stock funds — they’re your best long-term inflation hedge. That said, consider holding a fund that holds high-quality dividend-paying growth or value stocks. Granted, value funds like Equity-Income and large-cap blend funds like Dividend Growth have long been overshadowed by higher-flying large-cap growth funds whose hefty tech exposures have super-charged their returns.

But over the past three years, they’ve collectively been 30% riskier (more volatile) than the S&P 500. For its part, Dividend Growth (which underweights tech 31% to 38%, and whose performance accelerated in the past year) has kept pace with that group. And its risk is only 5% higher than the market. Paying quarterly income, its dividend yield as of June 30 was 1.8% versus 1.1% for the S&P 500.

Not to be overlooked is our well-diversified Growth & Income Model. Thirty percent less risky than the market, since its 12/31/93 inception through 2025, its 32-year average annual return is 8.7% versus 2.6% for CPI, which is similar to Balanced and Puritan.

As for RMDs and other systematic withdrawals from your retirement savings, retirees should probably assume that their "personal inflation" is more in line with the Fed’s PCE inflation gauge, and if necessary, consider lowering your withdrawals accordingly.

Needless-to-say, your best investment strategy is one you’ve planned with your financial planner or advisor. Our goal here is to raise your awareness to inflation and encourage taking steps to guard against it.

— John Bonnanzio